In thinking about how the transformative impact of AI might change the way we value goods and services, I started to think about how it might transfer value itself. Our current monetary system simply doesn’t make sense given the properties of money agents will require. Turns out after researching it’s a bit of a rabbit hole, so I’ve done my best here to run you through the current system, why it’s not suitable and what options we have in future.

Two AIs Walk Into a Restaurant

In December 2025, Fetch.ai announced what they called the world's first AI-to-AI payment. Two personal AI agents, one belonging to each user, coordinated a dinner plan, found a restaurant, secured a reservation through OpenTable and completed the payment. Both users were offline while this happened.

A dinner reservation. It’s a small thing, but it revealed a large problem.

When AI agents work together, who pays? How does value transfer between machines? A research agent hires a math agent to verify a calculation. A travel agent negotiates with a hotel agent on your behalf. Each requires value to move, but our current payment infrastructure assumes a human clicks "buy."

Google put it simply in a recent article: "2025 was the year we stopped chatting with AI and started treating it like an actual employee." And employees get paid. Employees also pay for things. But our economic infrastructure was designed by humans, for humans. You need KYC to open a bank account. Credit cards require creditworthiness. True settlement of funds takes days, sometimes longer if sending over international rails like SWIFT, which I have experienced personally.

What happens when an agent needs to pay another agent on the other side of the planet with a fraction of a cent for a millisecond of compute time? When millions of these transactions happen per second? Or when value needs to stream continuously. Think of a listener streaming music and paying by the second, with that value instantly splitting into the wallets of every artist, producer, and songwriter who worked on the track.

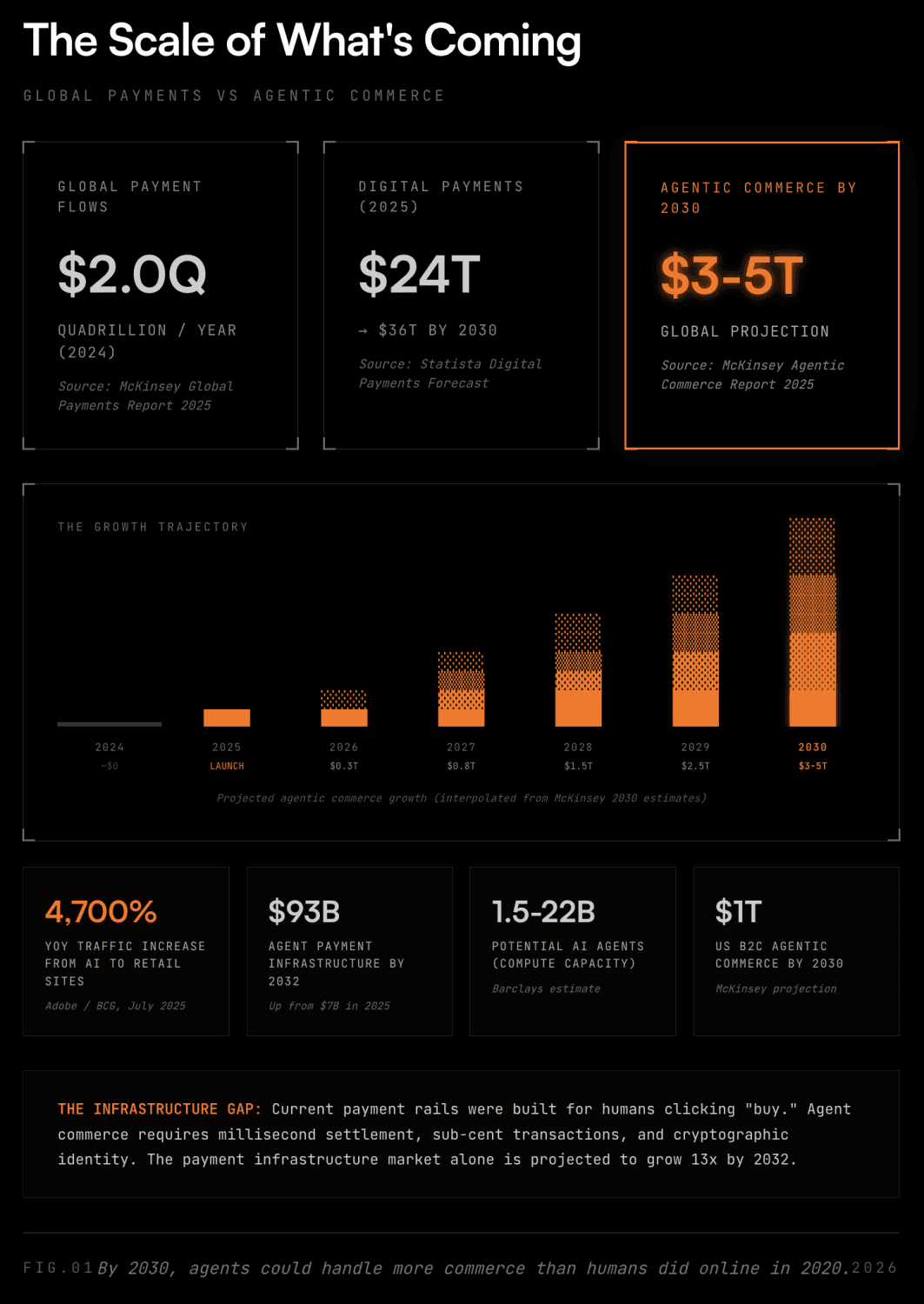

PayPal, Mastercard, Google, and Coinbase all launched agent payment infrastructure in 2025. McKinsey projects agentic commerce could handle $3-5 trillion globally by 2030. I think the thing I’ve realised after researching this article is that the plumbing is being laid right now, but mostly by people figuring out how to bolt AI onto existing rails rather than asking whether those rails make sense.

To work out the scale of the problem, I spent some time digging into how the current system actually works. I found a few things I think most people don't know.

How The Current System Actually Works

In November 1910, six men boarded a private railcar in New Jersey. They used first names only and told no one where they were going. The cover story: a duck hunting trip.

They headed to Jekyll Island, Georgia, to J.P. Morgan's private club and spent nine days designing what became the Federal Reserve: a privately owned central bank that could create money, set the price of borrowing, and bail out failing banks. They drafted it in secret because they knew the public wouldn't trust a banking system designed by bankers.

I should mention that this isn't a conspiracy theory. The Fed's own historians document it openly. But it helps to understand why they thought it was necessary.

Three years earlier, the Panic of 1907 had nearly collapsed the American financial system. Banks were failing in cascades and there was no central authority to stop the bleeding. So J.P. Morgan, a private citizen, personally organised the bailout by locking bankers in his library until they agreed to pool funds and stabilise the system. It worked, but Morgan was 70 years old at the time. The banking system needed a permanent solution. So six men went to an island and designed one.

The Federal Reserve Act was signed December 1913. Australia, like most Western economies, eventually adopted a similar model. The core architecture hasn't fundamentally changed since.

Here's what I found when I dug into how it actually works. You might not know this.

Central banks don't print money and hand it to commercial banks. Commercial banks create money through the act of lending. When a bank approves your mortgage, it doesn't transfer existing money from somewhere else. It creates new money out of thin air, a deposit in your account that didn't exist before. The money supply then expands. However, when you repay the principal, that deposit is extinguished and the money supply contracts. But the interest payments are different; that's the bank's profit.

So what do central banks actually do then? They decide, through a slow and very human process, how much money flows through the financial system by setting the price of borrowing (interest rates) which makes lending more or less attractive. The RBA's Monetary Policy Board meets eight times a year. Nine people, including the Governor, Deputy Governor, Treasury Secretary, and six external experts, look at quarterly GDP figures and monthly employment surveys, then decide interest rates for a $2.8 trillion economy. By the time they're analysing the data, it's already weeks or months old.

This is the operating system running beneath everything. Designed in 1910 and fundamentally unchanged for over a century.

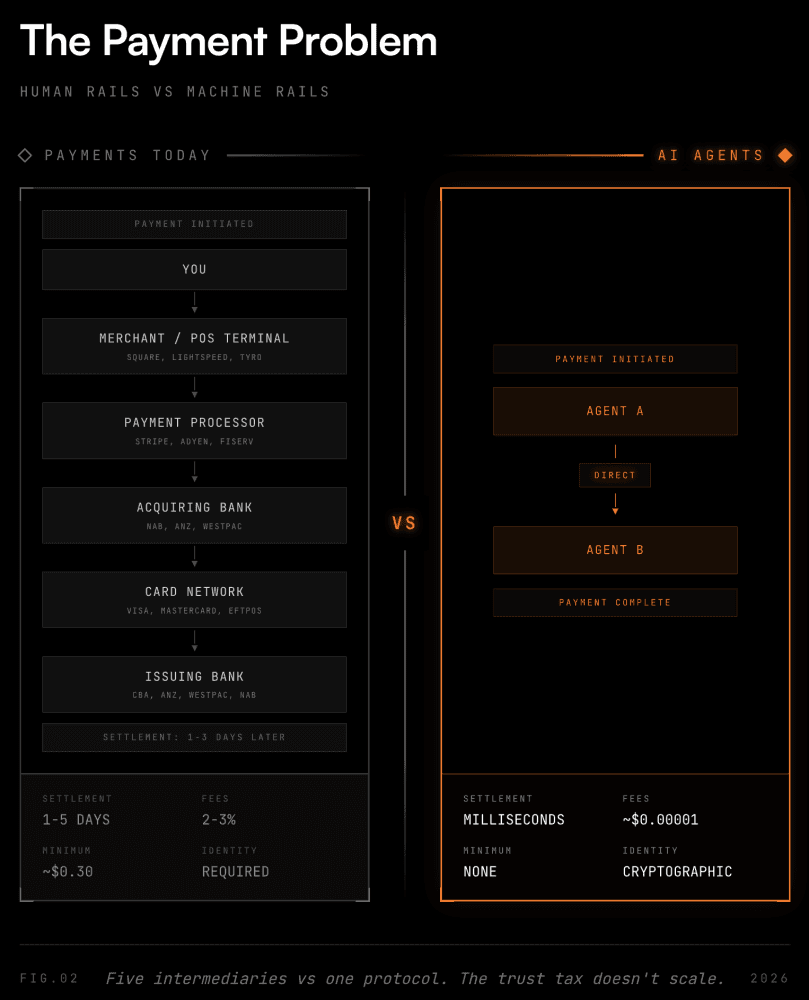

And on top of that century-old foundation? We've just kept stacking on it. Payment processors, card networks, acquiring banks, issuing banks, fraud detection layers, compliance checks. Each one added to solve a problem created by the last. Buy a coffee today and your $5 passes through five or six intermediaries before it settles, days later, minus a cut at every step.

Why It's Broken

"Broken" is probably too strong. The system arguably works. It's survived world wars and financial crises. But it was designed for a world that no longer exists. Here's what I see as the main cracks:

Speed. Central banks make decisions based on old data. The RBA meets eight times a year. But the economy moves faster. It's like steering a ship by looking at where it was last quarter.

Granularity. We don't measure the economy directly. Our metrics of GDP, employment, inflation are all approximations. They tell us roughly what happened, on average, some time ago. They can't tell us what's happening now.

Cost. Every transaction carries what I'd call a trust tax. Because we can't verify things directly, we need intermediaries like banks, card networks, and processors, each taking a cut. A $100 purchase might cost the merchant $3 in fees. For humans, 3% is annoying but we’ll swallow it. For AI agents making millions of sub-cent transactions per second, it's not viable at all.

Access. The system requires identity documents and bank accounts. AI agents don't have either.

None of these were problems in 1910. Transactions were human-paced and measurements were good enough because only humans needed to transact.

Why This Matters Now

2025 was the year AI agents entered payments. Not as a concept, but with real products.

PayPal launched agentic AI commerce. Mastercard unveiled Agent Pay. In September 2025 Google announced AP2, an open protocol with 60+ organisations. These aren't simple experiments either. These are proper pieces of production infrastructure.

Our current payment systems are built on the assumption that a human clicks "buy." Fraud detection looks for human behaviour, login patterns, typing speed, geographic consistency. Dispute resolution assumes someone can explain what happened and why. Tax frameworks assume a person is earning income and filing returns. When an AI agent transacts at machine speed, across jurisdictions, thousands of times per second, it’s becoming increasingly clear to me that none of these assumptions hold any more.

Here’s another interesting thought. A law firm analysis I found raised a question without answer:

"How can a merchant prove proper authorization and authentication when an AI agent initiated the payment transaction, rather than the cardholder personally?"

When an AI agent makes a bad purchase, who's responsible? The user? The developer? The AI itself? The courts haven't decided and the frameworks don't yet exist.

So What Are The Options?

There’s a lot at stake and it would seem different groups want different things from whatever comes next.

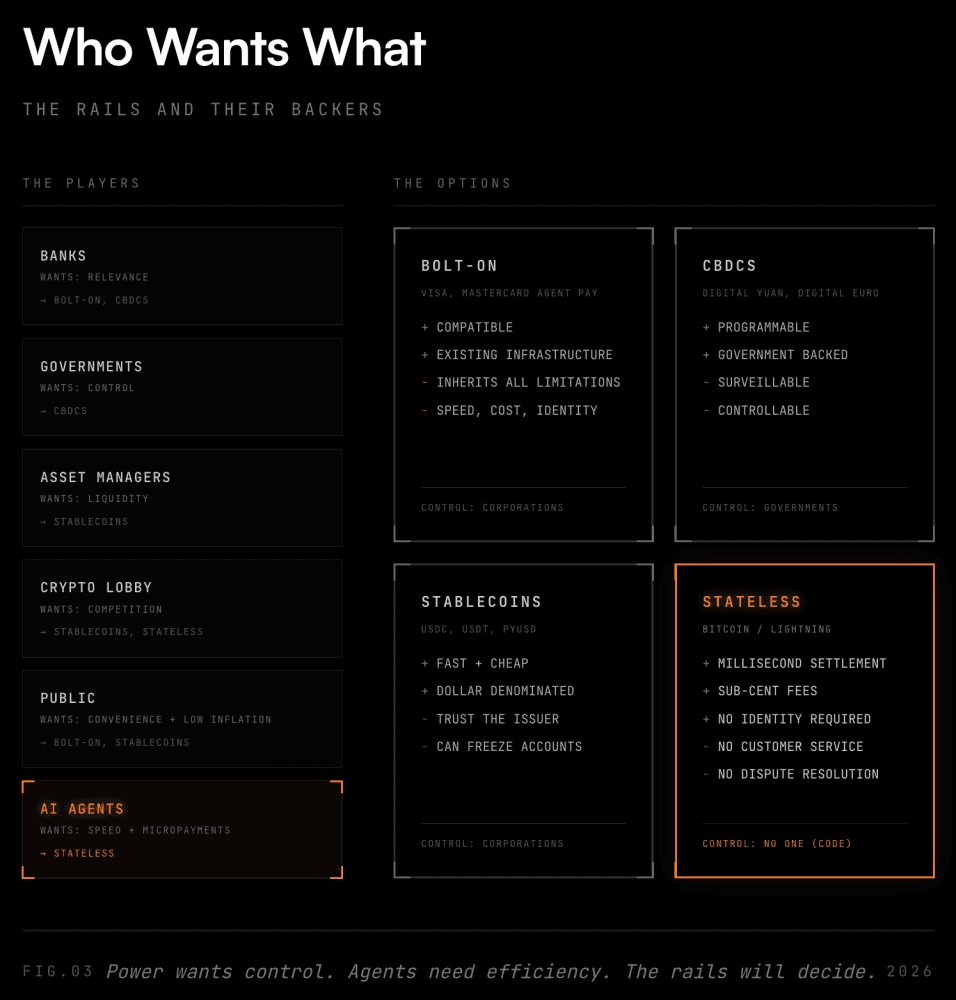

Asset managers want programmable money that moves instantly across borders. Banks want to stay relevant and not get cut out of the flow. Governments want control over their own economies. The crypto lobby wants fair competition, knowing they'd win in a level game. Each is pulling in a different direction, and each is building infrastructure to match. (Andrei Jikh has a great breakdown of these power structures if you want to go deeper.)

Each group is betting on their preferred outcome. But as I see it, every option comes with trade-offs.

The bolt-on approach (Visa's Trusted Agent Protocol, Mastercard's Agent Pay) extends existing infrastructure to handle agents. Compatible with current systems, but inherits all their limitations: speed, cost, identity requirements.

Central Bank Digital Currencies offer programmable government money. 137 countries are exploring them. But programmable money is also surveillable money, and controllable money. The US explicitly rejected CBDCs via legislation citing privacy concerns and China's own digital yuan includes transaction limits and expiry dates.

Stablecoins are private digital dollars. They offer speed and low cost, but you're trusting the issuer to hold the reserves. Centralised control with corporate rather than government fingerprints.

Stateless money like Bitcoin's Lightning Network enables sub-second settlement for fractions of a cent with no issuer, no accounts, no identity requirements. The payment itself serves as authentication. No one controls it. That's the feature and the limitation: no customer service, no dispute resolution, no one to call.

For machine-to-machine commerce, I think the trust question matters most. Agents transacting with agents don't need a bank vouching for identity. They need cryptographic proof. They don't need three-day settlement times. They need milliseconds. And they need to transact with fractions of a cent.

But something I haven't gotten my head around yet is who chooses which rails agents use? There’s a few ways this plays out.

Do the creators decide? OpenAI, Google, and Anthropic could hardcode their agents to use specific payment networks. That would give enormous power to whoever builds the most popular agents. Do the users decide? You might set preferences for your personal AI, but what about when your agent negotiates with thousands of other agents you've never heard of? Do the agents themselves decide? If agents optimise for speed and cost, they'll naturally gravitate toward whatever protocol has the least friction. Market forces, not policy, would pick the winner. That’s my view.

But the most likely answer is all three, at different layers. Your bank might mandate how your agent pays for things in your name. But when agents are transacting with each other, intermediaries add latency and cost that compounds across millions of interactions. So at machine scale, efficiency wins.

As an experiment I asked an AI what it would prefer if it were an agent making payments. Its answer was pretty blunt:

"For agent-to-agent transactions at scale, stateless rails fit the requirements best. Not because of ideology—because of physics. Latency and fees compound across millions of interactions. I don't have a passport. I can't fill out KYC forms. I need a system where the payment is the proof. The protocol with the least friction wins by default."

I liked the use of the em dash, that’s how you know it’s real AI. But take that with appropriate skepticism. It's an AI answering a hypothetical about AI preferences. I can’t argue with the logic though when I think about it. When you strip away the politics and the incumbents and ask what actually serves the technical requirements, the answer points in a specific direction. Work backwards from the need and stateless, permissionless rails seems to fit the bill.

Where This Is Headed

After researching all of this, it's obvious to me that an overhaul isn't optional, it's already being built.

Google, Mastercard, Coinbase, OpenAI are all racing to set standards. Coinbase's x402 protocol embeds stablecoin payments directly into HTTP. An agent hits a paywall and pays a fraction of a cent to get the data. No account, no session and no human. It's already processed 75 million transactions as of December 2025. On the stateless side, projects like Start With Bitcoin by Bram Kanstein are packaging identity, wallets, and Lightning payments into open-source toolkits that any developer can plug into an agent in minutes. I think the question is, given the option to decide for itself, what will an agent choose? They would seem to already prefer stateless methods like Bitcoin and Lightning.

As PYMNTS put it:

Protocols decide who owns the customer, who controls the economics, and who sets the rules.

In 1910, six men on a private island designed the system we still use. They were solving their era's problems: banking panics, fragmented currency, no lender of last resort. The problems now are different. Machine-speed transactions. Micropayments. Agent identity. Global coordination without intermediaries. The current operating system wasn't built for any of this. Something else will be. The only question is what, and who decides.